Executive Summary

Equities are down around 4% on the month and have drawn down around 6% from their highs now. US stocks have underperformed, while economically sensitive sectors have seen relatively more selling. The selloff has been driven by uncertainty around tariffs, with the blanket tariffs introduced by President Trump being met by reciprocal tariffs from China and other countries. The fear is that a trade war will negatively impact already fragile consumer sentiment and trigger a growth slowdown or even a recession.

VAR equity portfolios are positioned quite conservatively and have held up relatively well over the correction. We have a cash position of ~10%, having reduced exposure in late February, which has helped to cushion any declines. Within equity portfolios, our key overweights are to US equities and to technology, where we think there’s attractive earnings growth and where valuations are now more attractive following the correction. The best way to gain exposure to equities is through a diversified portfolio of our best ideas, which is what the current portfolio represents. We’re constantly working on new ideas to potentially add to the portfolio; however, the hurdle new ideas have to cover to make it into the portfolio is high.

What’s Been Happening in Markets?

To briefly summarise what has been happening, markets have been under pressure over most of March. The MSCI All-Country World index is down about 4% on the month (and about 7% from the highs); the US has suffered a bit more, with the S&P 500 down around 6% on the month and the Nasdaq down about 7%; Europe has fared better, with the Stoxx 600 declining a more modest 3%.

On a YTD basis, the All-Country World index has now declined almost 5%, while the S&P has declined about 5% as well, while the Nasdaq is now down over 9% on the year. European equities have performed very well, with the Stoxx 600 still up over 6% on the year in spite of the March declines; while the Nikkei has had a tough year, falling about 8%, we note that Asia Pacific equities overall have done well, and we note that Hong Kong equities in particular are doing very well, up 18% on the year to build on the gains we saw towards the end of last year based on optimism over activity from the CCP to support markets.

Finally on broad market performance, we’d note that the dollar has lost significant ground this year against EUR (~6%), JPY (~6%) and GBP (~4%), meaning that for holders of US stocks with their overall portfolios denominated in non-USD, there have likely been some quite meaningful currency headwinds to deal with if those portfolio are unhedged.

Looking at sector performance in March, the spread of growth relative to value stands out, with the S&P Value index down about 4.5%, while the S&P Growth index has had a more difficult period, declining about 8.5%. Digging a little deeper into sector performance, what we’re seeing is a rotation away from economically-sensitive sectors into more defensive names – in the US, Food, Beverages & Tobacco, Household Products, and Utilities have been among the best performers, while Autos, Banks and Tech Hardware have struggled. In Europe, we’ve seen more mixed evidence – while the economically-sensitive Retail, Travel, and Consumer Products sectors have been weak, we’ve noticed a certain willingness among investors to buy into sectors such as Construction and Chemicals (both of which are quite cyclical). We think some of that willingness is driven by Trump-related headlines, which we delve into below.

Picking up on that final observation and moving onto what’s been driving weakness in markets, probably the key drivers have been the combination of Trump-related headlines, along with an eagerness among investors to sell some of the outperformers from 2023 and 2024.

Looking first at the Trump headlines, the topic most top of mind for investors is tariffs. The blanket 25% tariffs on China and Canada took effect last week, with China swiftly responding with reciprocal tariff increases on US agricultural imports into their country. We’ve perceived a growing consensus among investors that the US President either doesn’t understand that tariffs could effectively work as a consumption tax on US consumers, or he doesn’t care. In terms of the first point, there’s been much discussion around the fact that the President seems not to understand that tariffs are ultimately paid for by consumers via passthroughs from importers, as opposed to by the governments of the countries from which the imports originate. The tariffs might thus end up working like a consumption tax – higher taxes generally act as a fiscal headwind, slowing the economy, and given that many surveys already point to quite fragile consumer sentiment, further flies in the ointment thrown in by the US government have likely heightened fears around a trade war-driven recession, weighing on risk assets.

We think it’s probably naive to think that a sitting President would fail to grasp how tariffs work, so we’d focus more on the argument around him understanding the downside and being willing to press ahead anyway. We’d point to President Trump’s interview with Fox News over the weekend, with the President acknowledging the risk around recession and seemingly making the argument that the short-term pain of a recession would justify the long-term gain. We’re also mindful of Treasury Secretary Bessent’s so-called “3/3/3” economic agenda of increasing US oil production by 3m barrels/day, reducing the budget deficit to 3% of GDP, and achieving 3% GDP growth. While the latter would probably be risk-positive if achieved, given the tax cuts seem to be non-negotiable for President Trump, it’s not clear how a reduction in the deficit with tax cuts would be achievable without taking a sickle to government spending (hence the DOGE-related headlines earlier in the year). A significant retrenchment in government spending was discussed as a downside risk in the aftermath of the election, but was largely dismissed by markets, however the recent price action and Fox News interview over the weekend seem to have refocused investors on recession risk, with tariff imposition now a reality.

Aside from tariff headlines, we have also seen other news flow driven by President Trump that has had a very different impact on European markets. We’re referring here to the ugly scenes in the White House from around two weeks ago, with Ukrainian President Zelensky berated by President Trump and Vice President Vance, effectively being told to either negotiate a ceasefire and concede territory or face the consequences. Markets were initially aghast at the prospect of the US no longer being a reliable foreign partner and US Exceptionalism potentially ending, however risk assets in Europe seem to have found their footing and have continued to outperform. As daunting as the prospect of Europe having to go it alone may sound, the German response was twofold:

- Proposing that any defence spending greater than 1% of GDP will be exempt from the debt brake

- To establish a €500bn infrastructure fund (to be used over 10 years) that will again be exempt from the debt brake

While these two measures represent probably the most significant event in German fiscal policy since the fall of the Berlin Wall, and the move lower in bunds reflects an assessment that German borrowing costs are likely to increase, they could theoretically boost economic growth in Germany (and by extension the rest of Europe), which has been received quite enthusiastically among European investors.

The newsflow overall has, however, been received as quite negative for risk assets. US bond markets have moved to price in relatively more rate cuts this year, and the yield curve has inverted – both moves can be interpreted as an attempt by markets to price in a relatively higher recession risk in the US. Investors have responded to that by selling of economically sensitive equities, along with those that have done well in recent years (semiconductor stocks would be a good example of a corner of the market vulnerable to both of those cross currents, probably explaining their ~12% YTD declines in the US).

What have we been doing, how have we done, how are we positioned?

We modestly reduced exposures within equity portfolios towards the end of February, which somewhat shielded us from recent declines. We sold out of two holdings entirely (AstraZeneca and Hasbro) and reduced two other holdings (S&P Global and Nestle).

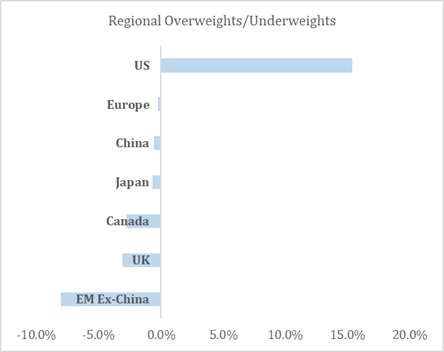

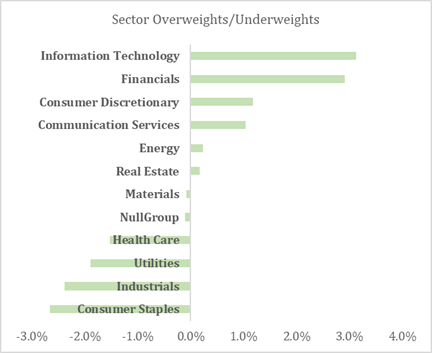

At a high level, we retain an overweight position in US equities, the majority of which is “funded” by an underweight to Emerging Markets Ex-China (we have a roughly market weight position in Chinese stocks). In terms of sector exposure, our key overweight remains to Information Technology (the Financials overweight is skewed by Berkshire Hathaway, which MSCI classifies as a Financial, but is in fact has a broader exposure), while we also retain a modest overweight to Consumer Discretionary via investments in companies such as Home Depot and LVMH. Our underweights are mainly in more defensive sectors such as Consumer Staples, Utilities, and Healthcare.

We summarise broad exposures for a representative portfolio below:

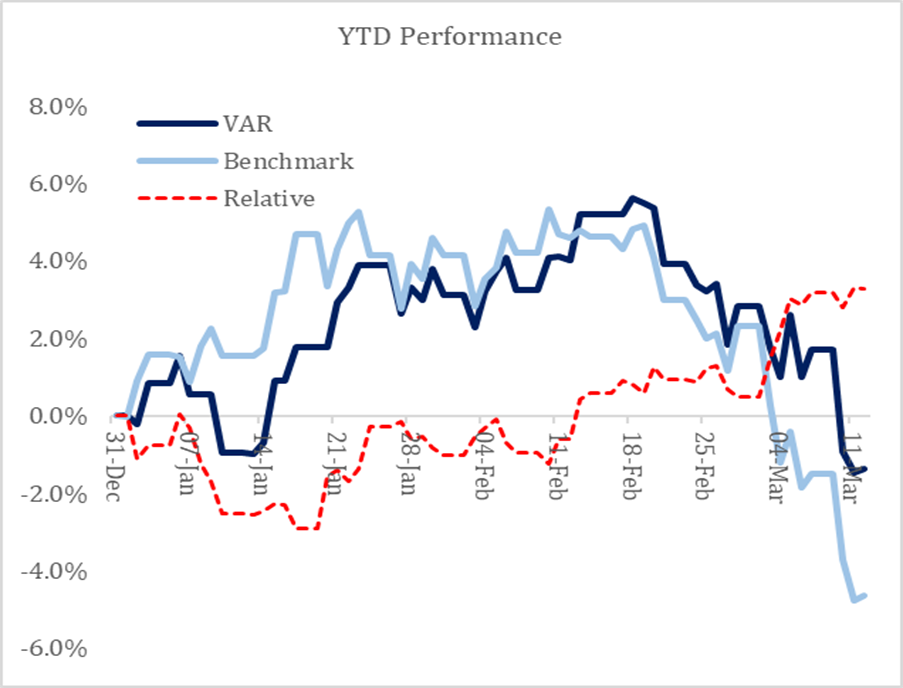

Generally speaking, regional and sector positioning has been a modest headwind for us over the selloff, most notably the overweight towards US stocks and the overweights in IT and Financials (even excluding Berkshire Hathaway). The US overweight headwind has been exacerbated by currency moves for non-USD portfolios, given the selloff we’ve seen in USD. That thematic positioning has been more than offset by stock picking, which has been a tailwind – notable winners have included Dassault Aviation, HCA Healthcare, Nestle, Verisign and Pernod Ricard. Below we summarise YTD performance for a representative portfolio relative to a benchmark that’s comparable (MSCI All-Country World Index rebased into GBP to remove the currency impact).

The dotted red line represents our relative performance, which has been positive. For the sake of clarity, one could argue that the USD overweight is an active asset allocation decision, and in the interests of full disclosure, not adjusting for the currency headwind, a representative portfolio has performed about in-line with the benchmark YTD.

What are we watching from here and what looks interesting?

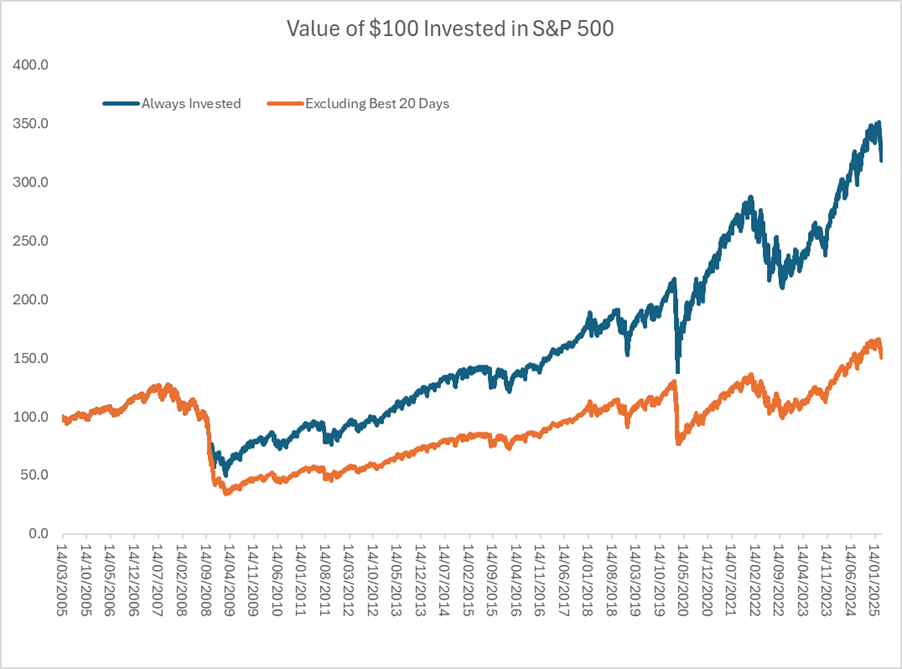

We would first counsel clients to maintain a long-term outlook and resist the temptation to try to get out of the market and wait for things to settle down. While superficially reasonable, the problem with this approach is that, like many things, equity returns follow a Pareto distribution (better known as the 80/20 rule) – namely, most of the returns come from just a few very good days. Below we illustrate returns from $100 invested in the S&P over the last 20 years, the blue line being the return from being invested 100% of the time, the orange line from being invested every day but the best 20 days over the last 20 years:

Source: Bloomberg, VAR Research

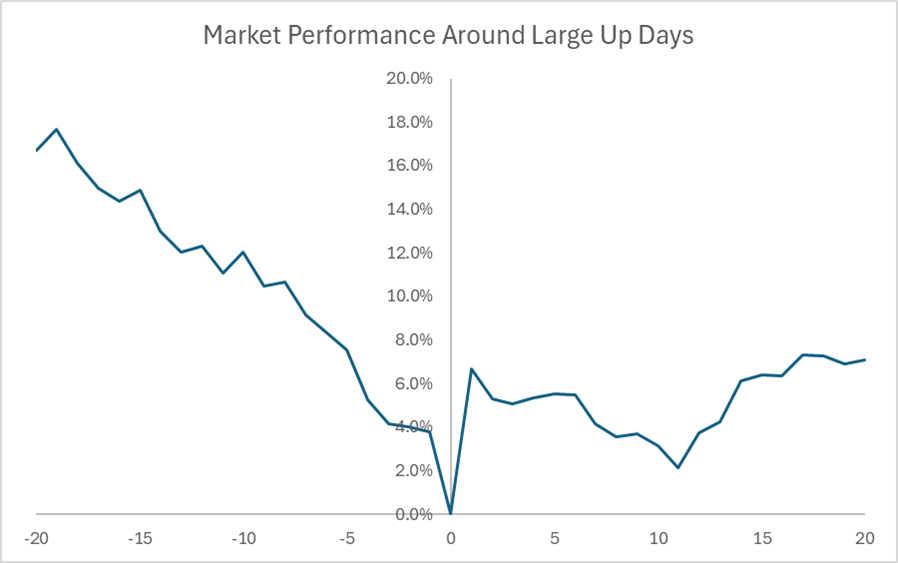

Being out of the market at the wrong time can be seriously detrimental to your financial health. While one might reasonably respond that you’d need to be very unlucky to be out of the market on those days, given they represent less than a half of one percent of all trading days, unfortunately, the big up days tend to come in the aftermath of very bad equity market performance in the 2-3 weeks leading up to the bounce

Source: Bloomberg, VAR Research

The general pattern here is that markets are weak, investors eventually become fatigued and feel they can’t take any more pain (which seems to take a few weeks), there is capitulation, followed by a very large up day after which markets seem to form a base off of which to build. While history doesn’t repeat, it often rhymes, and the analogies to what we’re seeing in markets now are not difficult to make.

In terms of what’s interesting to us – US equities have done poorly YTD, which has been painful for us given our positioning. We think there are a few things to be mindful of regarding US equities. Even after the recent selloff, valuations in the US look relatively demanding, both compared to long-term history (for instance cyclically adjusted P/E, or CAPE) and compared to equities in other regions such as Europe and Emerging Markets. That has been the case for most of the last decade, and we think for good reasons (to name just a couple – a higher proportion of the higher-quality companies with deep moats around them are listed in the US; the average US company has better corporate governance), however that does place a “burden of proof” on US companies. They need to show earnings growth to justify their valuations, and while consensus expectations are still quite rosy for S&P earnings growth (around double-digit EPS growth for 2025), those expectations have been tempered in the last couple of months. We’d also note that earnings growth has for the last couple of years been rather focused on a select group of companies (Magnificent 7 companies would be the key example here) and in fact earnings growth excluding these rapid growers has been rather more muted.

That dynamic, together with the growth fears we have referred to, would suggest that the best opportunities might lie outside of the US. While Europe and EM certainly look cheap, and we do own companies in those regions, we think it’s important to temper one’s enthusiasm somewhat. Companies outside the US tend to trade at discounts for a reason, for instance weaker end markets in Europe, generally poorer corporate governance with less regard for shareholders and more regard for other stakeholders in Europe and Japan, weaker legal protections and currency risk in EM. We own quality companies in Europe (ASML, LVMH for instance) and select EM (Alibaba for instance) and are open to owning more, however the hurdle to make it into the portfolio is high.

In terms of where we’d deploy money after the market selloff the current portfolio represents our best thinking and is something we’d be comfortable deploying new money into currently. There are always new opportunities to examine, and the market volatility that we’ve seen has thrown out many such opportunities. We’re working on many of those ideas at the moment, however the current portfolio represents a set of high conviction ideas, and the hurdle for new ideas to cover in order for us to deploy capital into them is high.

Note – figures as of the afternoon of 12th March

Disclaimer:

This message is provided for information purposes and should not be construed as a solicitation or offer to buy or sell any securities or related financial instruments, nor does the information constitute advice or an expression of our view as to whether a particular financial product is appropriate for you. Please note that we do not provide any tax or legal advice and clients must seek their own tax advice independently.

VAR Capital is an independent financial services firm offering asset management, lending and family office services. It was founded by individuals with extensive experience from Banking, Asset Management and Family Offices. Based in Mayfair, London, VAR Capital Ltd is authorised and regulated by the Financial Conduct Authority (FCA).

Source: VAR Capital

Media Contact: Vikash Gupta, [email protected]